Thursday, 31 January 2019

Sunday, 27 January 2019

"corporate governance zealots"

There's a bit of a daft bit in the Sunday Times today from Patience Wheatcroft. It argues that "corporate governance zealots" will drive directors of PLCs towards private equity, where there is less hassle/scrutiny. The argument is that we don't want to shackle our risk-takers in all that corporate governance red tape.

I say it's daft as this is really an auto-pilot moan. I first heard it when I was working about the TUC, which is well over a decade ago, and it pops up every now and then.

In fact, pretty much exactly the same argument appears in... err... the Sunday Times last February accusing... err... "corporate governance zealots" of... err... driving PLC directors towards private equity.

That piece was written by Luke Johnson, latterly most famous as executive chairman of Patisserie Valerie.

And say what you like about him, but he's clearly a risk taker.

Finally, it would be churlish to point out that the phrase "corporate governance zealots" has a bit of history in the newspaper business too. So I won't.

I say it's daft as this is really an auto-pilot moan. I first heard it when I was working about the TUC, which is well over a decade ago, and it pops up every now and then.

In fact, pretty much exactly the same argument appears in... err... the Sunday Times last February accusing... err... "corporate governance zealots" of... err... driving PLC directors towards private equity.

That piece was written by Luke Johnson, latterly most famous as executive chairman of Patisserie Valerie.

And say what you like about him, but he's clearly a risk taker.

Finally, it would be churlish to point out that the phrase "corporate governance zealots" has a bit of history in the newspaper business too. So I won't.

Saturday, 26 January 2019

BlackRock short position in AA Plc

I find this weirdly fascinating. At 4.61% Blackrock's short in AA Plc is by far its largest current short position. The second largest is half the size - 2.26% in Go-Ahead Group. And it's been steadily heading up over the past year.

I think it's Blackrock's largest short in a UK stock since the FCA has started disclosing major short positions. It is now larger than the peak short position it had in Carillion (4.4%). Mitie is the only other company where it has taken a position anywhere near this large (that peaked at 3.8%) according to the FCA historical shorts list.

It's the largest current short in AA Plc held by any manager and by a long way. (Big shorts total 9.14%, but there are bound to be more below 0.5%)

It's also one of the largest current short positions held by any manager in any UK stocks.

Ho hum.

I think it's Blackrock's largest short in a UK stock since the FCA has started disclosing major short positions. It is now larger than the peak short position it had in Carillion (4.4%). Mitie is the only other company where it has taken a position anywhere near this large (that peaked at 3.8%) according to the FCA historical shorts list.

It's also one of the largest current short positions held by any manager in any UK stocks.

Ho hum.

Thursday, 24 January 2019

Stock-lending and shorting, again

I've been thinking a bit more about the potential conflicts of interest around stock-lending and shorting in light of the RD:IR paper I blogged about a couple of weeks back. It suggested that passive managers are in part able to offer lower fees because they make money through stock-lending.

I was initially interested in the way that this might facilitate shorting on the cheap by the active side of the same business. If you're managing passive assets on a large scale on an AUM-based fee then I think you can probably lend to your active side safe in the knowledge that even if they call it right the decline in one stock isn't going to rock the boat (NB - I'm not saying shorting makes share prices decline!). I think that is still worth digging into, just to find out a) how extensive lending by passive managers is b) how much the passive clients make out of it and c) if cross-group lending is done, and, if so, if it's charged at a cheaper rate than to external clients.

But what interests me is what other issues might arise. I am reminded of this bit from an old Takeover Panel paper about the conflicts created for counterparties to derivatives in bid situations:

If you oppose the bid, and it fails, it's quite possible that stock-lending clients will lose a bundle. If so, will they come back to you as a borrower next time? I have heard anecdotes about borrows being sniffy about lenders who want to recall to vote, so I could imagine some conflicts / client pressure.

Another area to dig into...

I was initially interested in the way that this might facilitate shorting on the cheap by the active side of the same business. If you're managing passive assets on a large scale on an AUM-based fee then I think you can probably lend to your active side safe in the knowledge that even if they call it right the decline in one stock isn't going to rock the boat (NB - I'm not saying shorting makes share prices decline!). I think that is still worth digging into, just to find out a) how extensive lending by passive managers is b) how much the passive clients make out of it and c) if cross-group lending is done, and, if so, if it's charged at a cheaper rate than to external clients.

But what interests me is what other issues might arise. I am reminded of this bit from an old Takeover Panel paper about the conflicts created for counterparties to derivatives in bid situations:

First, the Code Committee believes that, notwithstanding the contractual arrangements between them, a counterparty will usually know the derivative investor’s likely wishes and therefore it would be naïve to assume that the counterparty (who has no economic interest in any hedge securities it holds but who does have an ongoing client relationship with the investor) will act without having some regard to those wishes. In addition, as indicated in paragraph 3.3 of PCP 2005/1, the Code Committee understands that it is frequently the expectation of a long derivative investor, notwithstanding the terms of the documentation, that his counterparty will ensure that the securities to which the derivative is referenced are available to be voted by the counterparty and/or sold to the investor on closing out the contract. If the counterparty does not hold any such securities (because, for example, its book is balanced by an offsetting short derivative), the investor would normally expect the counterparty to acquire the necessary securities, even if that resulted in a cost to the counterparty.…..the Panel continues to encounter situations where holders of long derivative positions behave as if they were shareholders and, more importantly, situations where investment bank counterparties enquire of investors with long derivative positions as to their preferences in terms of bid outcomes in order that the counterparties may take those preferences into account;Do similar issues arise for passive managers who stock-lend? Say you're a regular lender to funds doing the merger arbitrage trade. Say a big contentious hostile bid comes up and your lending clients have taken a big punt shorting the acquirer in the expectation that the bid succeeds. Is there any tension in how you decide to respond to the deal? Big passive managers are going to be long in both target and acquirer. I'm pretty sure there must be an optimum outcome in this situation, but if your positions are passive (so you're not being judged on performance) I suspect you've got freedom of movement to decide how to respond.

If you oppose the bid, and it fails, it's quite possible that stock-lending clients will lose a bundle. If so, will they come back to you as a borrower next time? I have heard anecdotes about borrows being sniffy about lenders who want to recall to vote, so I could imagine some conflicts / client pressure.

Another area to dig into...

Infrastructure investment politics 2

I've blogged a couple of times before about the political challenges facing investment in infrastructure. In the last couple of days there have been a couple more news stories that show how sharp these issues are getting.

First up, the FT ran a piece about overseas institutional investors putting a "blanket ban" on investing in UK infrastructure. Essentially this is due to political (and therefore regulatory) risk and, importantly, investors say this is no longer restricted to Labour policy:

Then today Reuters ran a piece about investors seeking creative ways to protect their existing investments in UK infrastructure against the threat of renationalisation:

Nonetheless, these the high-level politics around public ownership are pretty straightforward now. Few MPs are going to see much sense in fighting to defend the right of Macquarie to run a UK water company. No political party is going to run a "defend privatised utilities!" campaign - at best they will silent, though eve those who are ambivalent are more likely to criticise (like Gove) thus making it easier for others to act. And that's pretty scary for investors.

First up, the FT ran a piece about overseas institutional investors putting a "blanket ban" on investing in UK infrastructure. Essentially this is due to political (and therefore regulatory) risk and, importantly, investors say this is no longer restricted to Labour policy:

Investors point to the effect that opposition leader Jeremy Corbyn has had on the government, which has adopted some Labour policies. This includes the surprise decision to abolish the future use of the private finance initiative in last year’s Autumn statement as well as environment secretary Michael Gove’s criticism of the privatised water companies, which he accused of “playing the system for the benefit of wealthy managers and owners”. “What Corbyn has achieved is a reaction within other parties,” one infrastructure investor told the FT. “There is no one in the political arena defending us any more.”I think the point about their being no political support for private ownership is particularly telling.

Water bosses were startled at a conference in November when a senior Conservative politician, Sir Oliver Letwin, appeared to express indifference as to whether the sector was in private or public hands.

Then today Reuters ran a piece about investors seeking creative ways to protect their existing investments in UK infrastructure against the threat of renationalisation:

Some major shareholders in water companies are seeking to safeguard their investments from nationalization should the left-wing Labour Party win power, by shifting their stakes to holding companies in Hong Kong, according to investment industry and legal sources with knowledge of the matter.As I blogged before, the fact that these stories are appearing tells you something in itself. People are talking about, and planning for, changes to public policy around the ownership of infrastructure assets. There obviously remain significant obstacles to major changes to ownership in practice. Until a political party committed to change takes power, critical words about private ownership might be all the action that there is. In addition, the cost of renationalisation remains... err... large, and its benefits may not be strongly felt.

Funds including Australia’s IFM Investors are aiming to take advantage of a bilateral investment treaty between Britain and Hong Kong designed to protect against state expropriation of assets, the sources told Reuters.

Nonetheless, these the high-level politics around public ownership are pretty straightforward now. Few MPs are going to see much sense in fighting to defend the right of Macquarie to run a UK water company. No political party is going to run a "defend privatised utilities!" campaign - at best they will silent, though eve those who are ambivalent are more likely to criticise (like Gove) thus making it easier for others to act. And that's pretty scary for investors.

Sunday, 20 January 2019

Loyalty: a few initial thoughts

This tweet from Which? caught my eye the other day, and is something I've been thinking about a lot lately:

The tweet (which is currently pinned!) referred to the cost of sticking with the same broadband providers, and it reminded me of a similar tweet from ex Adam Smith Institute dude Sam Bowman before xmas:

And when I Googled "loyalty doesn't pay" I found other examples with the same message, like this:

In a way there's nothing new here. You'd expect advocates of market forces to argue that people (consumers) should move around rather than being "loyal" to a particular provider. They are typically very attached to "exit" as a discipline.

And obviously it's good advice on one level. There's not much point being loyal to an energy provider if you're paying more than using a competitor. If the amount involved is big enough to overcome the faff involved in switching it makes sense.

In the corner of the world that I inhabit, loyalty is not a prized value either. In fact incentives for loyalty are extremely unpopular. A significant case for me was DSM back in 2007. The company was seeking to introduce a loyalty dividend so that if you held the shares for longer you got slightly higher dividends. But it was attacked by asset managers and eventually scrapped.

At the time I was surprised, these days I am not surprised at all. A subsequent report on loyalty incentives by Mercer and Generation issued in 2013 found institutional investors opposed to loyalty rewards:

I would argue that there has been a similar development in employment. Many employers have sought to shed their obligations to their workforce and they increasingly seek to deny an "employment" relationship at all. One of the most interesting books I read last year was The End Of Loyalty by Rick Wartzman (nice review here), which is all about the changing relationship between employers and employees (and their unions) from the immediate post-war period to the present day. The big theme is that as organised labour's power diminished so employers became less willing to offer long-term security to employees. Loyalty was undermined. Notably, he also sees the shift to shareholder value / shareholder primacy as part of the explanation.

Finally - and perhaps this is a bit of a reach - I personally find complaints from politically active and knowledgeable people that they are "politically homeless" a bit jarring. To me, they come across as betraying quite an entitled and transactional mindset - a political party should align with all my views and values or it cannot count on my vote. There's a great quote about politics that I read some time last year which was along the lines that loyalty that doesn't cost anything is meaningless.

I think there's a lot in all this worth exploring but here are a few initial thoughts. I think that to many actually existing humans, loyalty is an admirable quality, not something to be discouraged. Loyalty is at the core of some of the things we care most about. We actively profess loyalty to our football team, or our country, or our political party and, yes, sometimes even to brands and products. What's more, we demonstrate (and measure) loyalty by the length of our commitment and by what we endure along the way. We respect those who suffer for their support and loyalty, and denigrate those who only profess allegiance in the good times and/or go missing when it gets tough. In political/moral psychology, loyalty/betrayal is one of the pillars in the moral foundations theory associated with Jonathan Haidt.

Yet look at that Which? tweet again. Yes, there is a context but the message is very very clear: loyalty costs you, it's a self-defeating trait. I wonder what kind of reaction this creates. My gut feeling is that, rather than eliminating the concept of loyalty in this field (presumably the objective), it engenders distrust. If loyalty is a concept with which I make sense of the world (and likely it's part of my mental make-up for evolutionary reasons, so it's not something I can just "switch off"), and I discover (or am told, in this instance) that certain organisations will take advantage of my loyalty then I am not going to think highly of them. If I learn/am taught that my loyalty will be exploited by an entire sector (insurance companies, in Sam Bowman's tweet), I am likely to conclude that the whole sector will betray me and therefore cannot be trusted. I think it's less likely that I will conclude that my sense of loyalty is the problem.

When I look at the way that institutional shareholders react to loyalty rewards - which some would no doubt consider to be economically rational - I wonder what the reaction in turn of the humans working for companies like DSM is. Again, my gut feeling is that it suggests - or confirms - that you shouldn't trust asset managers. I think this is why the question of asset managers shorting their own clients jars with me. I don't believe that the human beings who are executives at the companies being shorted simply think "fair enough, that's how the systems operates, and they have Chinese walls". I think it will sting emotionally, at least some of them. I know some of them consider institutional shareholders to be entirely mercenary.

And in the world of employment, I suspect that we are still only starting to see the counter-reaction to the reduction of employer loyalty to employees. In the past a lot of employees felt some loyalty to their employer, it was part of their identity. But, if you read a book like Hired you can see that sense of loyalty is gone, along with social clubs and defined benefit pensions. If millennial workers don't trust employers (because of the lack of loyalty) we perhaps can't be surprised if they demand a lot to come onboard / stay onboard, because they expect to get shafted.

So perhaps the widespread distrust in institutions at least in part results from the violation of loyalty. And emphasising the desirability of "exit" - and the foolishness of remaining loyal - exacerbates this. (I think there is a link to the idea of self-interest as a norm, that I blogged about a few years back.)

Anyway, I think this is a theme I'll be blogging about more in future.

The tweet (which is currently pinned!) referred to the cost of sticking with the same broadband providers, and it reminded me of a similar tweet from ex Adam Smith Institute dude Sam Bowman before xmas:

And when I Googled "loyalty doesn't pay" I found other examples with the same message, like this:

In a way there's nothing new here. You'd expect advocates of market forces to argue that people (consumers) should move around rather than being "loyal" to a particular provider. They are typically very attached to "exit" as a discipline.

And obviously it's good advice on one level. There's not much point being loyal to an energy provider if you're paying more than using a competitor. If the amount involved is big enough to overcome the faff involved in switching it makes sense.

In the corner of the world that I inhabit, loyalty is not a prized value either. In fact incentives for loyalty are extremely unpopular. A significant case for me was DSM back in 2007. The company was seeking to introduce a loyalty dividend so that if you held the shares for longer you got slightly higher dividends. But it was attacked by asset managers and eventually scrapped.

At the time I was surprised, these days I am not surprised at all. A subsequent report on loyalty incentives by Mercer and Generation issued in 2013 found institutional investors opposed to loyalty rewards:

Respondents identified four main obstacles in utilising loyalty rewards as a means to overcome the root cause of the short term pressures found in the full investment chain: 1 – Discrimination between shareholders due to belief in “1 share, 1 vote” 2 – Risk of unintended consequences 3 – Administrative complexities 4 – Uncertainty that loyalty driven securities would incent a significant change in behaviour and address the root causes of short-termismJust to be absolutely clear: investors oppose rewards for loyalty on principle even though they have the potential to gain from them. They do not want to see "exit" disincentivised (relatively). Perhaps views have changed in the 6 years since the Mercer report, but I doubt it.

I would argue that there has been a similar development in employment. Many employers have sought to shed their obligations to their workforce and they increasingly seek to deny an "employment" relationship at all. One of the most interesting books I read last year was The End Of Loyalty by Rick Wartzman (nice review here), which is all about the changing relationship between employers and employees (and their unions) from the immediate post-war period to the present day. The big theme is that as organised labour's power diminished so employers became less willing to offer long-term security to employees. Loyalty was undermined. Notably, he also sees the shift to shareholder value / shareholder primacy as part of the explanation.

Finally - and perhaps this is a bit of a reach - I personally find complaints from politically active and knowledgeable people that they are "politically homeless" a bit jarring. To me, they come across as betraying quite an entitled and transactional mindset - a political party should align with all my views and values or it cannot count on my vote. There's a great quote about politics that I read some time last year which was along the lines that loyalty that doesn't cost anything is meaningless.

I think there's a lot in all this worth exploring but here are a few initial thoughts. I think that to many actually existing humans, loyalty is an admirable quality, not something to be discouraged. Loyalty is at the core of some of the things we care most about. We actively profess loyalty to our football team, or our country, or our political party and, yes, sometimes even to brands and products. What's more, we demonstrate (and measure) loyalty by the length of our commitment and by what we endure along the way. We respect those who suffer for their support and loyalty, and denigrate those who only profess allegiance in the good times and/or go missing when it gets tough. In political/moral psychology, loyalty/betrayal is one of the pillars in the moral foundations theory associated with Jonathan Haidt.

Yet look at that Which? tweet again. Yes, there is a context but the message is very very clear: loyalty costs you, it's a self-defeating trait. I wonder what kind of reaction this creates. My gut feeling is that, rather than eliminating the concept of loyalty in this field (presumably the objective), it engenders distrust. If loyalty is a concept with which I make sense of the world (and likely it's part of my mental make-up for evolutionary reasons, so it's not something I can just "switch off"), and I discover (or am told, in this instance) that certain organisations will take advantage of my loyalty then I am not going to think highly of them. If I learn/am taught that my loyalty will be exploited by an entire sector (insurance companies, in Sam Bowman's tweet), I am likely to conclude that the whole sector will betray me and therefore cannot be trusted. I think it's less likely that I will conclude that my sense of loyalty is the problem.

When I look at the way that institutional shareholders react to loyalty rewards - which some would no doubt consider to be economically rational - I wonder what the reaction in turn of the humans working for companies like DSM is. Again, my gut feeling is that it suggests - or confirms - that you shouldn't trust asset managers. I think this is why the question of asset managers shorting their own clients jars with me. I don't believe that the human beings who are executives at the companies being shorted simply think "fair enough, that's how the systems operates, and they have Chinese walls". I think it will sting emotionally, at least some of them. I know some of them consider institutional shareholders to be entirely mercenary.

And in the world of employment, I suspect that we are still only starting to see the counter-reaction to the reduction of employer loyalty to employees. In the past a lot of employees felt some loyalty to their employer, it was part of their identity. But, if you read a book like Hired you can see that sense of loyalty is gone, along with social clubs and defined benefit pensions. If millennial workers don't trust employers (because of the lack of loyalty) we perhaps can't be surprised if they demand a lot to come onboard / stay onboard, because they expect to get shafted.

So perhaps the widespread distrust in institutions at least in part results from the violation of loyalty. And emphasising the desirability of "exit" - and the foolishness of remaining loyal - exacerbates this. (I think there is a link to the idea of self-interest as a norm, that I blogged about a few years back.)

Anyway, I think this is a theme I'll be blogging about more in future.

Friday, 18 January 2019

More short stuff

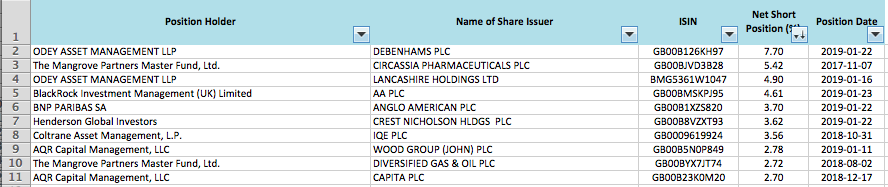

Again, huge caveat that the data in these charts is only 0.5%+ short positions, but some interesting stuff I think. At the end of play yesterday the FCA had disclosed 581 current short positions of 0.5% and above in UK shares. So I looked at which firms had the most shorts, and - of that group - what their average, median and largest short positions were.

Blackrock has the most shorts in total, and also the second largest individual short of the sample. Odey has the largest single short and average short. AQR has the largest median short, second largest average short and third largest individual short.

A rough (and pretty obvious) reading of this is that the hedge funds that make shorting a significant part of their strategy take a small number of bigger positions. I am surprised by the sheer number of Blackrock shorts (and there must be a lot more under 0.5%) which makes me wonder if a lot of this is hedging. Also quite surprised to see both JP Morgan Asset Management and Merian Global Investors (formerly Old Mutual) in the mix.

For info I had an arbitrary way of picking firms - just those with 10 or more shorts in the list.

PS - 20 largest shorts and the funds that have them:

Blackrock has the most shorts in total, and also the second largest individual short of the sample. Odey has the largest single short and average short. AQR has the largest median short, second largest average short and third largest individual short.

A rough (and pretty obvious) reading of this is that the hedge funds that make shorting a significant part of their strategy take a small number of bigger positions. I am surprised by the sheer number of Blackrock shorts (and there must be a lot more under 0.5%) which makes me wonder if a lot of this is hedging. Also quite surprised to see both JP Morgan Asset Management and Merian Global Investors (formerly Old Mutual) in the mix.

For info I had an arbitrary way of picking firms - just those with 10 or more shorts in the list.

PS - 20 largest shorts and the funds that have them:

Thursday, 17 January 2019

Even More Duplicate Reporting 2: The Boilerplate Strikes Back

Neptune (looks like an old statement, but hey)

We will continue any dialogue with the company over an extended period where deemed necessary. Escalation of our engagement activities, including any engagement with other investors, will depend on the company’s individual circumstances and the nature of the concerns identified.

......

Neptune recognises that in many instances joint action by shareholders has the potential to be more effective than acting alone. This is especially the case where shareholders have a clear common interest, such as in times of significant corporate or wider economic stress, or when the risks posed threaten to destroy significant value. Neptune will pursue opportunities for collaborative engagement in such circumstances and will engage with other investors through formal and informal groups when it is necessary to achieve their objectives and ensure companies are aware of concerns.

......

Neptune fund managers and research analysts maintain regular dialogue with companies which forms part of their research notes published internally to the investment team. This communication allows Neptune to monitor the development of companies in areas such as; overall strategy; leadership; business planning; capital structure, including any internal or external developments that may drive the company’s value and risk; company reporting; proposed acquisitions or disposals; and corporate responsibility and governance.

River & Mercantile

We will continue our dialogue with the company over an extended period if necessary. Escalation of our engagement activities will depend upon the company’s individual circumstances. Actions may include communications through the company’s brokers, direct engagement with the chairman or non-executive directors or joint intervention with other shareholders, and where appropriate, voting against board proposals

....

We recognise that in many instances joint action by shareholders has the potential to be more effective than acting alone. This is especially so where shareholders have a clear common interest and at critical moments. Our policy is to pursue opportunities for collaborative engagement in such circumstances. In considering participation in collaborative engagement initiatives we take into account potential conflicts of interest, concert party rules and our policy on insider information.

......

RAMAM’s fund managers and analysts maintain regular dialogue with companies. This dialogue allows us to monitor the development of companies’ businesses, including areas such as overall strategy, business planning and delivery of objectives, capital structure, proposed acquisitions or disposals, corporate responsibility and corporate governance. In addition, we engage with other stakeholders to enhance our own views on company performance. Whilst we may attend company general meetings, our preference is for meeting one-on-one with companies.

Nomura (another old one?)

We will continue our dialogue with the company over an extended period if necessary. Escalation of our approach will depend upon the company's individual situation, and the country and jurisdiction to which it belongs. Escalated action might include communication through the board of directors or through channels other than our usual contacts.

NAM’s portfolio managers, research analysts and corporate governance specialists maintain regular dialogue with the companies into which they invest on behalf of clients. These communications allow us to evaluate key factors determining our investment decisions, such as the development of companies’ business operations, capital structures and financial standings, and strategic plans; as well as to monitor essential elements concerning a company’s sustainability, such as corporate governance and corporate social responsibility activities. We believe this continuous dialogue with companies will encourage them to give due consideration to their corporate responsibilities.

Napier Park

We will continue our dialogue with the company over an extended period if necessary.

......

Napier Park recognise that in certain instances joint action by shareholders has the potential to be more effective than acting alone. This is especially so where shareholders have a clear common interest, such as in times of corporate distress. Our policy is to pursue opportunities for collaborative engagement in such circumstances.

Napier Park’s fund managers and analysts maintain regular dialogue with companies within their particular business sphere. Such dialogue allows them to monitor the development of companies’ businesses, including areas such as overall strategy, business planning and delivery of objectives, capital structure, proposed acquisitions or disposals, corporate responsibility and corporate governance.

We will continue any dialogue with the company over an extended period where deemed necessary. Escalation of our engagement activities, including any engagement with other investors, will depend on the company’s individual circumstances and the nature of the concerns identified.

......

Neptune recognises that in many instances joint action by shareholders has the potential to be more effective than acting alone. This is especially the case where shareholders have a clear common interest, such as in times of significant corporate or wider economic stress, or when the risks posed threaten to destroy significant value. Neptune will pursue opportunities for collaborative engagement in such circumstances and will engage with other investors through formal and informal groups when it is necessary to achieve their objectives and ensure companies are aware of concerns.

......

Neptune fund managers and research analysts maintain regular dialogue with companies which forms part of their research notes published internally to the investment team. This communication allows Neptune to monitor the development of companies in areas such as; overall strategy; leadership; business planning; capital structure, including any internal or external developments that may drive the company’s value and risk; company reporting; proposed acquisitions or disposals; and corporate responsibility and governance.

River & Mercantile

We will continue our dialogue with the company over an extended period if necessary. Escalation of our engagement activities will depend upon the company’s individual circumstances. Actions may include communications through the company’s brokers, direct engagement with the chairman or non-executive directors or joint intervention with other shareholders, and where appropriate, voting against board proposals

....

We recognise that in many instances joint action by shareholders has the potential to be more effective than acting alone. This is especially so where shareholders have a clear common interest and at critical moments. Our policy is to pursue opportunities for collaborative engagement in such circumstances. In considering participation in collaborative engagement initiatives we take into account potential conflicts of interest, concert party rules and our policy on insider information.

......

RAMAM’s fund managers and analysts maintain regular dialogue with companies. This dialogue allows us to monitor the development of companies’ businesses, including areas such as overall strategy, business planning and delivery of objectives, capital structure, proposed acquisitions or disposals, corporate responsibility and corporate governance. In addition, we engage with other stakeholders to enhance our own views on company performance. Whilst we may attend company general meetings, our preference is for meeting one-on-one with companies.

Nomura (another old one?)

We will continue our dialogue with the company over an extended period if necessary. Escalation of our approach will depend upon the company's individual situation, and the country and jurisdiction to which it belongs. Escalated action might include communication through the board of directors or through channels other than our usual contacts.

NAM’s portfolio managers, research analysts and corporate governance specialists maintain regular dialogue with the companies into which they invest on behalf of clients. These communications allow us to evaluate key factors determining our investment decisions, such as the development of companies’ business operations, capital structures and financial standings, and strategic plans; as well as to monitor essential elements concerning a company’s sustainability, such as corporate governance and corporate social responsibility activities. We believe this continuous dialogue with companies will encourage them to give due consideration to their corporate responsibilities.

Napier Park

We will continue our dialogue with the company over an extended period if necessary.

Escalation of our engagement activities will depend upon the company’s individual circumstances. Actions may include communications through the company’s brokers, direct engagement with the chairman or non-executive directors or joint intervention with other shareholders, and where appropriate, voting against board proposals.

......

Napier Park recognise that in certain instances joint action by shareholders has the potential to be more effective than acting alone. This is especially so where shareholders have a clear common interest, such as in times of corporate distress. Our policy is to pursue opportunities for collaborative engagement in such circumstances.

......

Tuesday, 15 January 2019

Even more duplicate reporting...

Well, here's something. In a previous blog I noted that Liontrust Asset Management is apparently both a Tier 1 and a Tier 2 signatory of the Stewardship Code (though the statement is the same in both links).

Well, I had a bit of a Google around and I found that the Liontrust statement on the Stewardship Code bears more than a passing resemblance to a Martin Currie statement: GOVERNANCE OVERSIGHT OF INVESTEE COMPANIES AND PROXY VOTING

A couple of examples below.

Liontrust:

Martin Currie:

Liontrust:

Martin Currie:

Ho hum.

Here's another one. Try sticking the following into Google without quotes "The materiality and immediacy of a given issue will generally determine the level of our engagement"

I don't know where that sentence came from, and perhaps just a coincidence. But look at this Blackrock paper and this ValueCap stewardship statement.

Blackrock:

ValueCAP:

Thankfully the lack of a mechanistic process is also referenced in ValueCAP's PRI reporting.

Well, I had a bit of a Google around and I found that the Liontrust statement on the Stewardship Code bears more than a passing resemblance to a Martin Currie statement: GOVERNANCE OVERSIGHT OF INVESTEE COMPANIES AND PROXY VOTING

A couple of examples below.

Liontrust:

Martin Currie:

Liontrust:

Martin Currie:

Ho hum.

Here's another one. Try sticking the following into Google without quotes "The materiality and immediacy of a given issue will generally determine the level of our engagement"

I don't know where that sentence came from, and perhaps just a coincidence. But look at this Blackrock paper and this ValueCap stewardship statement.

Blackrock:

ValueCAP:

Thankfully the lack of a mechanistic process is also referenced in ValueCAP's PRI reporting.

More hedge fund cut 'n' paste fun

I had some fun last year exposing the boilerplate blah that many hedge funds (and a few bigger firms) were using to "explain" their non-compliance with the Stewardship Code. Many thanks to Responsible Investor for recently giving this a plug.

Anyway, I thought I'd have another look. In the list we submitted to the FRC and FCA last year, I had found 34 examples using pretty much the same text. So are there any more out there? Yes. Loads.

Below are some I didn't find first time around. I haven't included all the blurb - the full text includes words to describe their approach to engagement with issuers which, miraculously, seems to be the same across dozens of firms. Incidentally, a couple of the URLs are interesting. One uses the word "template" and another includes "UK_Stewardship_Code_Applicable_BUT_firm_chooses_NOT__to_commit_and_explains_why"

These are just from the first three pages of Google results (even I get bored of this stuff). There are a lot more.

Somerset Capital Management:

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to it.

Marine Capital (this one looks reasonable, to be fair):

MCL invests directly in shipping assets and therefore it has no exposure to UK listed companies. Therefore, whilst MCL generally supports the objectives that underlie the Code, the nature of its investment strategy makes it impractical and unnecessary to engage with investee companies through voting rights. The Firm has therefore chosen not to commit to the Code at this time.

Baker Steel

Consequently, while the Firm supports the general objectives that underlie the Code, the Firm has chosen not to commit to the Code. Given the investment strategies of the Funds, the principles of the Code are generally not relevant to the type of trading currently undertaken by the Firm. If the Firm's investment strategy changes in such a manner that the provisions of the Code become relevant, the Firm will amend this disclosure accordingly.

Sagil Capital

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

Pamplona Capital Management

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen to not commit to the Code.

Avenue Capital (this is the one that includes "template" in the Google results)

As such, while the Firm generally supports the objectives that underlie the Code, the Firm does not consider it appropriate to commit to any particular voluntary code of practice relating to any individual jurisdiction.

Hadron Capital

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

Blue Whale

While Blue Whale supports the objectives that underlie the Code, Blue Whale is not in a position to commit to the Code in its entirety.

Nextam Partners

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

AKO Capital

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

Partners Group

Whilst PGUK generally supports the objectives that underlie the Code, it has chosen not to commit to the Code at this time.

Clearance Group

While the firm generally supports the objectives that underlie the Code, the firm has chosen not to commit to the Code.

Edgbaston Investment Partners

Whilst Edgbaston generally supports the objectives that underlie the Code, it does not consider it appropriate to commit to any code of practice relating to any individual jurisdiction.

Markham Rae

Consequently, while the Firm supports the objectives that underlie the Code, the provisions of the Code are not relevant to the type of investment currently undertaken by the Firm.

RAB Capital

While RAB generally supports the objectives that underlie the Code, it has chosen not to commit to the Code.

Atlas Square

Hence, while the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

KAM Portfolio Management

While the firm generally supports the objectives that underlie the Code, KAM has chosen not to commit to it.

Glen Point

While the firm generally supports the objectives that underlie the Code, Glen Point has chosen not to commit to the Code.

Sturgeon Capital

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

Anyway, I thought I'd have another look. In the list we submitted to the FRC and FCA last year, I had found 34 examples using pretty much the same text. So are there any more out there? Yes. Loads.

Below are some I didn't find first time around. I haven't included all the blurb - the full text includes words to describe their approach to engagement with issuers which, miraculously, seems to be the same across dozens of firms. Incidentally, a couple of the URLs are interesting. One uses the word "template" and another includes "UK_Stewardship_Code_Applicable_BUT_firm_chooses_NOT__to_commit_and_explains_why"

These are just from the first three pages of Google results (even I get bored of this stuff). There are a lot more.

Somerset Capital Management:

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to it.

Marine Capital (this one looks reasonable, to be fair):

MCL invests directly in shipping assets and therefore it has no exposure to UK listed companies. Therefore, whilst MCL generally supports the objectives that underlie the Code, the nature of its investment strategy makes it impractical and unnecessary to engage with investee companies through voting rights. The Firm has therefore chosen not to commit to the Code at this time.

Baker Steel

Consequently, while the Firm supports the general objectives that underlie the Code, the Firm has chosen not to commit to the Code. Given the investment strategies of the Funds, the principles of the Code are generally not relevant to the type of trading currently undertaken by the Firm. If the Firm's investment strategy changes in such a manner that the provisions of the Code become relevant, the Firm will amend this disclosure accordingly.

Sagil Capital

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

Pamplona Capital Management

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen to not commit to the Code.

Avenue Capital (this is the one that includes "template" in the Google results)

As such, while the Firm generally supports the objectives that underlie the Code, the Firm does not consider it appropriate to commit to any particular voluntary code of practice relating to any individual jurisdiction.

Hadron Capital

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

Blue Whale

While Blue Whale supports the objectives that underlie the Code, Blue Whale is not in a position to commit to the Code in its entirety.

Nextam Partners

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

AKO Capital

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

Partners Group

Whilst PGUK generally supports the objectives that underlie the Code, it has chosen not to commit to the Code at this time.

Clearance Group

While the firm generally supports the objectives that underlie the Code, the firm has chosen not to commit to the Code.

Edgbaston Investment Partners

Whilst Edgbaston generally supports the objectives that underlie the Code, it does not consider it appropriate to commit to any code of practice relating to any individual jurisdiction.

Markham Rae

Consequently, while the Firm supports the objectives that underlie the Code, the provisions of the Code are not relevant to the type of investment currently undertaken by the Firm.

RAB Capital

While RAB generally supports the objectives that underlie the Code, it has chosen not to commit to the Code.

Atlas Square

Hence, while the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

KAM Portfolio Management

While the firm generally supports the objectives that underlie the Code, KAM has chosen not to commit to it.

Glen Point

While the firm generally supports the objectives that underlie the Code, Glen Point has chosen not to commit to the Code.

Sturgeon Capital

While the Firm generally supports the objectives that underlie the Code, the Firm has chosen not to commit to the Code.

Saturday, 12 January 2019

The challenge (to unions) of pension fund 'socialism'

The Unseen Revolution by Peter Drucker is (like the Modern Corporation and Private Property) one of those books that has had a big influence on the world in which I inhabit, but also which is often misunderstood. Lots of people have probably heard the basic idea - that through the equity held by pension funds workers essentially "own" companies, and therefore we have a form of latent "socialism" if people would just wake up to it.

There are some obvious problems with even the outline - shareholders own shares not companies; not all pension schemes hold equity; pension fund coverage in many countries is skewed by class, gender and so on, so not everyone is a meaningful shareholder in practice; and day to day many pension funds act like any other financial market participants and aren't really friends of labour.

Nonetheless the basic idea is one that many on the Left are interested in and many people (me included) have spent years trying to make something like it meaningful.

But back to Drucker. Because a lot of people only know the outlines of the argument, they miss a lot of the really insightful stuff he wrote about the challenges that pension fund equity ownership creates. One of the most interesting bits is about the dilemma faced by trade unions, and to me Drucker seems to find this dilemma quite enjoyable. So here are some chunks of it.

As I regularly argue, we would be better off acknowledging the conflicts here, and thinking about how they should be worked through. I know very few investors who are anywhere near this yet, but I think this is where the hard work will need to be done in the coming years.

PS - the thing that people often overlook about the Modern Corporation and Private Property is that Berle and Means conclude that the diffusion of share ownership (and thus control) means that corporations should be accountable to 'the community'. Yet the book is often cited in support of the need for companies to be accountable to shareholders.

There are some obvious problems with even the outline - shareholders own shares not companies; not all pension schemes hold equity; pension fund coverage in many countries is skewed by class, gender and so on, so not everyone is a meaningful shareholder in practice; and day to day many pension funds act like any other financial market participants and aren't really friends of labour.

Nonetheless the basic idea is one that many on the Left are interested in and many people (me included) have spent years trying to make something like it meaningful.

But back to Drucker. Because a lot of people only know the outlines of the argument, they miss a lot of the really insightful stuff he wrote about the challenges that pension fund equity ownership creates. One of the most interesting bits is about the dilemma faced by trade unions, and to me Drucker seems to find this dilemma quite enjoyable. So here are some chunks of it.

Whatever the role of the labour union under pension fund socialism, it has to decide among equally dangerous alternatives, each challenging its cohesion.Well, we know how this turned out. Unions have generally not sought to represent employees as "owners". No rival organisations have materialised to fill the gap, rather the influence that derives from equity ownership has largely accreted to financial intermediaries (asset managers). Overall the balance of power has significantly shifted since Drucker was writing away from labour and towards capital (and it is the latter interest that is given pride of place in today's corp gov). But the the power of capital is not utilised by those to whom it belongs. Both companies and asset managers act as if the capital belongs to the latter, and its influence is used to advance the interests of capital, not labour.

The employees - the people whose organisation the labour union asserts itself to be and whom it claims to represent - are now increasingly both "employees" and "owners". Increasingly, they have an interest both in their job and its wage or salary, and in the performance and the profitability of enterprise. And increasingly, they stand in two relationships to the "system", which according to union logic and union rhetoric are mutually exclusive.

The labour movement can choose to ignore pension fund socialism. This would be the normal reaction for an American union leader - who does not challenge the "system" as such, but demands that one interest in it, that of the employee as employee, be given pride of place... The second alternative for labour is to try to use pension fund socialism as a means to expand union power by becoming the representative of the employees in their role as principal owners...

If America labour chooses to ignore the emergence of pension fund socialism, it runs therefore the one risk no trade union can possibly afford: the risk of a competing organisation's claiming to represent the employee. For if the union does not assume responsibility for the employee as owner, some other organisation will do so sooner or later. Such an organisation might take half a dozen different forms, but in any form it would be a competitor to the labour union. It would be an organisation of "labour" - not representing the employee as an employee against management, but ownership against management and employees alike...

The second alternative is equally risky: to accept pension fund socialism and to assert the labour union's role as representing the employee as owner. This would force the union into taking enterprise's even even management's side against the employee. The interest of the employee as an owner is by no means identical, at least not in the short run, with the interest of the employee as an employee. To an "employee", "profits" are something that is being "taken away from the worker," always seen as enormous and surely "excessive." To an "owner," on the other hand, profits are absolutely necessary; they are, in effect, the foundation of his future security. Instead of being excessive or exorbitant, they will almost always been seen as inadequate. To the employee, "productivity" is a dirty word... To an owner, "productivity" is what he pays management for.

As I regularly argue, we would be better off acknowledging the conflicts here, and thinking about how they should be worked through. I know very few investors who are anywhere near this yet, but I think this is where the hard work will need to be done in the coming years.

PS - the thing that people often overlook about the Modern Corporation and Private Property is that Berle and Means conclude that the diffusion of share ownership (and thus control) means that corporations should be accountable to 'the community'. Yet the book is often cited in support of the need for companies to be accountable to shareholders.

Shorting and stock-lending

Via LinkedIn (sorry!) I came across this interesting paper from RD:IR on what's going on with regards to stock-lending in the UK. Definitely worth a quick read for anyone with an interest in this area.

A couple of headline - the overall level of lending of UK stocks decreased after the crash, but has been rising since 2015. However this is driven by lending of FTSE250 stocks rather than FTSE100. At least part of the explanation appears to be Brexit, with lending in the FTSE250 increasing significantly post June 2016 (and the FTSE250 being generally a better representation of "UK" companies).

Although the paper makes clear that not all lending is to facilitate shorting, nonetheless it's clear that is what the bulk of it is for. As such there is a snapshot of who is doing the shorting:

Also, as a comparison, here are the largest 20 UK shorts disclosed on the FCA list as of Friday.

Marshall Wace, AQR and Blackrock are all in there, though no BNP Paribas.

Another interesting point in the paper is the the interplay between quant funds and passive managers, and, in particular, the importance of the latter in facilitating lending:

I keep returning to this, because something about all this makes me uneasy and I'm not quite sure what it is and why. Anyway, one for another day.

PS - I am pretty much convinced that the FCA should disclose all short positions that are reported to it. I appreciate this will make for a bigger list (and thus more admin). But 0.5%+ is a big hurdle.

A couple of headline - the overall level of lending of UK stocks decreased after the crash, but has been rising since 2015. However this is driven by lending of FTSE250 stocks rather than FTSE100. At least part of the explanation appears to be Brexit, with lending in the FTSE250 increasing significantly post June 2016 (and the FTSE250 being generally a better representation of "UK" companies).

Although the paper makes clear that not all lending is to facilitate shorting, nonetheless it's clear that is what the bulk of it is for. As such there is a snapshot of who is doing the shorting:

As at 20 November 2018, there were 609 disclosed short positions greater than 0.5%, totalling £13.4bn. The biggest “shorters” in UK Plc were Marshall Wace with £1.4bn, AQR Capital Management with £1.3bn, and BNP Paribas with £925m total shorts open and disclosed to the FCA. BlackRock, across its various global entities, held £896m in open short positions above 0.5%.This is based on FCA disclosures, which means the actual levels will be higher (because there will be a lot of short positions between 0 an 0.5% and some of them will be held by the big players). As noted in the previous example of Kier Group, the total shorts were more than double those disclosed in the FCA list, according to other data sources.

Also, as a comparison, here are the largest 20 UK shorts disclosed on the FCA list as of Friday.

Marshall Wace, AQR and Blackrock are all in there, though no BNP Paribas.

Another interesting point in the paper is the the interplay between quant funds and passive managers, and, in particular, the importance of the latter in facilitating lending:

One of the key reasons for the ability of passive investors to charge lower fees than active managers is the additional revenue stream of securities lending. This activity may seem contradictory to the classic view of investment, as you would invest into a certain sector/index via an EFT or index fund in the hope that your investment will increase in value. However, the fund manager or custodian for that fund may well at the same time be providing the market with shares from that fund’s portfolio to allow other investors to go short in that portfolio’s constituents.

The rise in passive investing via index and quant funds is fuelling shorting and stocklending. Quant funds are a driving force in the activity, with algorithms automatically opening short positions because of the sheer size of the lending market. At the end of 2017 the global market of tradable assets stood at more than $20tn, with over 10% of this total being lent out. The European market alone generated revenues of $2.6tn. Expectations are that 2018 produced even higher figures and 2019 more so. Of course, it is not just passive investment managers that are providing the liquidity in the lending market, with active managers seeking additional returns to cover falling fees in the ultra-competitive asset management market.Once again, my eye is drawn to Blackrock. They are both a major passive manager and a major player on the short side. If they want to short stocks they need to borrow them, so does the passive business lend to the bits of the business that go short, and if so do they charge the same rate they would do to other managers looking to short?

I keep returning to this, because something about all this makes me uneasy and I'm not quite sure what it is and why. Anyway, one for another day.

PS - I am pretty much convinced that the FCA should disclose all short positions that are reported to it. I appreciate this will make for a bigger list (and thus more admin). But 0.5%+ is a big hurdle.

Friday, 11 January 2019

Rights issues and rump placings

Before xmas, Kier Group held a rights issue which was something of a flop, with only about a third of the shares being taken up. The left the underwriters and sub-underwriters on the hook, and there was a subsequent "rump placing" that saw them dump a lot of stock below the issue price.

I've never really looked at this, so thought I'd trawl regulatory disclosures to see how Kier Group compared to others. Below are the disclosed percentages of stock that ended up at rump placings from 2015 to 2018. These figures are taken from regulatory filings that relate to rump placings and run from most recent on the far left, through to start of 2015 on the far right (including the dates made it very messy).

In most cases the amounts involved (the shares not taken up) are pretty trivial. During that period, only five got into double figures and only two saw more than 50%. In fact, Kier Group is only beaten by Petropavlovsk in terms of lack of take-up, and then only just, which is hardly great company if you've followed the story of that company. (The other noticeable spike is Lonmin, with 29% not taken up).

Interested to hear from anyone who knows this stuff better than I do if there is anything that I'm missing.

I've never really looked at this, so thought I'd trawl regulatory disclosures to see how Kier Group compared to others. Below are the disclosed percentages of stock that ended up at rump placings from 2015 to 2018. These figures are taken from regulatory filings that relate to rump placings and run from most recent on the far left, through to start of 2015 on the far right (including the dates made it very messy).

In most cases the amounts involved (the shares not taken up) are pretty trivial. During that period, only five got into double figures and only two saw more than 50%. In fact, Kier Group is only beaten by Petropavlovsk in terms of lack of take-up, and then only just, which is hardly great company if you've followed the story of that company. (The other noticeable spike is Lonmin, with 29% not taken up).

Interested to hear from anyone who knows this stuff better than I do if there is anything that I'm missing.

Tuesday, 8 January 2019

Stewardship Code duplication

Last year I blogged about the duplicate text that lots of hedge funds were using to "explain" their non-compliance with the Stewardship Code. It's still out there, and on a recent trawl I managed to find more examples of funds using the same blurb. But as no-one really seems to police this stuff on the regulatory side, it's just sitting there.

The other day when I was looking for ESG contacts at a couple of asset managers I don't know well I started looking through the Stewardship Code statements on the FRC's website. I noticed that I'd obviously hit one of these links (Loomis Sayles) on a previous trawl, but I also spotted that the manager is listed as both a Tier 1 and Tier 2 signatory (see below).

Actually, as you can see, both Loomis Sayles and Liontrust are listed in both Tier 2 and Tier 1. The link for the former lands in a slightly different place (which isn't actually a Stewardship Code statement) to the latter, though it's only a click away. In the case of Liontrust the links in both Tier 1 and Tier 2 go to the same document (it's the same URL I think).

And there's a third. Castlefield Investment Partners also appears in Tier 2 and Tier 1, though in the first case it's a dead link.

It's interesting that the Kingman Review (see below) was pretty sceptical about the impact of the Stewardship Code in practice and critical of the focus on policy statements. I'm not sure I completely agree overall, my own experience on the policy statement side is that there is some crap out there but no-one seems that fussed.

The other day when I was looking for ESG contacts at a couple of asset managers I don't know well I started looking through the Stewardship Code statements on the FRC's website. I noticed that I'd obviously hit one of these links (Loomis Sayles) on a previous trawl, but I also spotted that the manager is listed as both a Tier 1 and Tier 2 signatory (see below).

Actually, as you can see, both Loomis Sayles and Liontrust are listed in both Tier 2 and Tier 1. The link for the former lands in a slightly different place (which isn't actually a Stewardship Code statement) to the latter, though it's only a click away. In the case of Liontrust the links in both Tier 1 and Tier 2 go to the same document (it's the same URL I think).

And there's a third. Castlefield Investment Partners also appears in Tier 2 and Tier 1, though in the first case it's a dead link.

It's interesting that the Kingman Review (see below) was pretty sceptical about the impact of the Stewardship Code in practice and critical of the focus on policy statements. I'm not sure I completely agree overall, my own experience on the policy statement side is that there is some crap out there but no-one seems that fussed.

Shire takeover & derivatives

So the takeover of Shire PLC by Takeda Pharma has been completed. I thought I'd have a quick look for merger arbitrage plays in the filings.

A few familiar names in the list below. Most of these investors are listed as having an interest (presumably short) in Takeda too and I've found a couple of examples:

Millennium - 0.68% in shares, 2.28% in derivatives

York Capital - 1.51% in derivatives

Marshall Wace - 0.3% in shares, 0.7% in derivatives

DE Shaw - 0.54% in shares, 1.07% in derivatives (Takeda short here)

Davidson Kempner - 1.39% in shares

UBS O Connor - 1.03% in derivatives

HBK Investments - 0.17% in shares, 3.08% in derivatives

Elliott - 0.0002% [chuckle] in shares, 1.28% in derivatives (Takeda short here)

This is just from a quick Google. Final positions may have been high/lower. But doesn't take long to get to 10%+ interest through derivatives.

A few familiar names in the list below. Most of these investors are listed as having an interest (presumably short) in Takeda too and I've found a couple of examples:

Millennium - 0.68% in shares, 2.28% in derivatives

York Capital - 1.51% in derivatives

Marshall Wace - 0.3% in shares, 0.7% in derivatives

DE Shaw - 0.54% in shares, 1.07% in derivatives (Takeda short here)

Davidson Kempner - 1.39% in shares

UBS O Connor - 1.03% in derivatives

HBK Investments - 0.17% in shares, 3.08% in derivatives

Elliott - 0.0002% [chuckle] in shares, 1.28% in derivatives (Takeda short here)

This is just from a quick Google. Final positions may have been high/lower. But doesn't take long to get to 10%+ interest through derivatives.

Friday, 4 January 2019

Gigged: a new old story

One of the books I've read over the holiday period is Gigged by Sarah Kessler. It's a quick read, nicely written and manages to get across some important points.

First up, if you're reading the book from labour-oriented perspective you may find the start of the book a bit unsettling. There are a series of stories about individual gig workers that run through the book, and in the early stages these are positive. People talk about the freedom and flexibility associated with gig/platform work, and the ability to get started and start earning quickly.

I bet a lot of people who share similar views to me will be thinking (yeah... but....!) while reading this. I know I did. But I think that it's really important that those of us who are interested in working practices, and changes to them, never lose sight of the fact that these are the real emotional responses of real gig workers. The picture is complicated, but people who do this work do find positives relative to traditional employment.

Second, that said, in almost all the individual cases the stories turn sour. Workers find it hard to make the kind of money that they were promised (Uber drivers in particular), experience a level of control more associated with normal employment etc (an important point here is the difficulty in changing unpleasant features of apps etc) and so on.

Another point here is that support for "flexibility" is linked to how well you are likely to do. If you're a highly-skilled worker it all looks good. If you're on Mechanical Turk tagging photos for pennies, or an Uber driver making a few quid an hour after costs, it's not so great.

Third, a lot of gig working looks a lot like poor employment practices in other bits of the economy. Here's a good example of a guy call Gary who worked as a customer services call centre operator from his home, picking up jobs online:

Similarly, the way that the work is pitched to workers doesn't really differ much from how temp agencies pitched to female workers decades ago. And the model of seeking an arm's length relationship workers, paying them only for work done with no formal employment or commitment to benefits etc is obviously not new.

Fourth, a lot of the gig economy companies didn't set out thinking of themselves as employers, and have struggled to come to terms with employment relationships. What comes across in the book quite strongly from the story of Managed by Q, is that tech start-ups just didn't think about these issues at all. They just thought about technology. I don't think this is a justification for their employment model, and obviously subsequently companies have had a choice how to address these questions. I don't think you can look at Uber now and think it doesn't know exactly what the issues are, it is simply trying to protect its model for as long as possible.

Fifth, that said, some gig economy employers have shifted towards a more traditional employment model (ie they actually employ workers) and have made it work. There is a decent section on the Good Jobs Strategy here (which doesn't really include unions...). Labour costs go up, but so does retention, motivation etc. This seems worthy of more investigation

Sixth, unions are in the mix, but primarily in shifting the model back towards formal employment. There are quite a lot of references to unions throughout the book - in terms of gig worker interest in them, union reactions to gig work, policy ideas and so on. But there aren't good examples of unions managing to represent gig workers effectively. This is probably partly because the book is largely US-focused and partly because of the difficulties in independent contractors taking collective action. Where unions have made a few dents is in successfully challenging the employment status of gig workers.

Overall there is still little agreement on the way forward. Most of the big gig economy players do not want to change their model, and their proposals on issues such as portable benefits are (again in the US context) very limited. They seem to be quite happy sticking to the "workers like flexibility and being their own boss" mantra. Business-friendly politicians and regulators do not want to intervene significantly (the UK's Taylor Review is a good example). I suspect until there is more policy intervention there will be a slow grind of legal cases (like the challenges to Uber all over the world) that end up determining employment relationships. This seems like a highly unsatisfactory way to decide the future of work, especially when the corporates have deep coffers they are willing to use to defend their model.

First up, if you're reading the book from labour-oriented perspective you may find the start of the book a bit unsettling. There are a series of stories about individual gig workers that run through the book, and in the early stages these are positive. People talk about the freedom and flexibility associated with gig/platform work, and the ability to get started and start earning quickly.

I bet a lot of people who share similar views to me will be thinking (yeah... but....!) while reading this. I know I did. But I think that it's really important that those of us who are interested in working practices, and changes to them, never lose sight of the fact that these are the real emotional responses of real gig workers. The picture is complicated, but people who do this work do find positives relative to traditional employment.

Second, that said, in almost all the individual cases the stories turn sour. Workers find it hard to make the kind of money that they were promised (Uber drivers in particular), experience a level of control more associated with normal employment etc (an important point here is the difficulty in changing unpleasant features of apps etc) and so on.

Another point here is that support for "flexibility" is linked to how well you are likely to do. If you're a highly-skilled worker it all looks good. If you're on Mechanical Turk tagging photos for pennies, or an Uber driver making a few quid an hour after costs, it's not so great.

Third, a lot of gig working looks a lot like poor employment practices in other bits of the economy. Here's a good example of a guy call Gary who worked as a customer services call centre operator from his home, picking up jobs online:

Imagine a nesting doll with Gary at the centre: Gary was the smallest doll, and independent contractor working for the [Independent Business Operator]. Go one layer bigger, and you'd see the IBO (the small business that hired Gary). Another layer bigger, and you'd see Arise, the big customer service company that had made a contract with the IBO. Only after another layer would you find Sears, the company that the customer thought he was dealing with.This multi-level supply chain is the same that you see in transport (delivery for example).

Similarly, the way that the work is pitched to workers doesn't really differ much from how temp agencies pitched to female workers decades ago. And the model of seeking an arm's length relationship workers, paying them only for work done with no formal employment or commitment to benefits etc is obviously not new.

Fourth, a lot of the gig economy companies didn't set out thinking of themselves as employers, and have struggled to come to terms with employment relationships. What comes across in the book quite strongly from the story of Managed by Q, is that tech start-ups just didn't think about these issues at all. They just thought about technology. I don't think this is a justification for their employment model, and obviously subsequently companies have had a choice how to address these questions. I don't think you can look at Uber now and think it doesn't know exactly what the issues are, it is simply trying to protect its model for as long as possible.

Fifth, that said, some gig economy employers have shifted towards a more traditional employment model (ie they actually employ workers) and have made it work. There is a decent section on the Good Jobs Strategy here (which doesn't really include unions...). Labour costs go up, but so does retention, motivation etc. This seems worthy of more investigation

Sixth, unions are in the mix, but primarily in shifting the model back towards formal employment. There are quite a lot of references to unions throughout the book - in terms of gig worker interest in them, union reactions to gig work, policy ideas and so on. But there aren't good examples of unions managing to represent gig workers effectively. This is probably partly because the book is largely US-focused and partly because of the difficulties in independent contractors taking collective action. Where unions have made a few dents is in successfully challenging the employment status of gig workers.

Overall there is still little agreement on the way forward. Most of the big gig economy players do not want to change their model, and their proposals on issues such as portable benefits are (again in the US context) very limited. They seem to be quite happy sticking to the "workers like flexibility and being their own boss" mantra. Business-friendly politicians and regulators do not want to intervene significantly (the UK's Taylor Review is a good example). I suspect until there is more policy intervention there will be a slow grind of legal cases (like the challenges to Uber all over the world) that end up determining employment relationships. This seems like a highly unsatisfactory way to decide the future of work, especially when the corporates have deep coffers they are willing to use to defend their model.

Tuesday, 1 January 2019

Infrastructure investment politics

A couple of stories caught my eye over the last few days, both relating to the ownership of infrastructure.

The first piece is from the FT and looks at the dividends paid to the owners of the UK's airports. This contrasts the amounts paid to shareholders and the debt issued. It also suggests friction between airport owners and airlines, with some moans about airport owners taking out dividends rather than investing in their infrastructure or reducing landing charges. I am unclear to what extent any of these moans are a) new or b) more of a general howl of pain from carriers.

However, I assume this piece has not come out of the blue. Someone has been complaining. And it's notable too that this piece is in the same sort of vein as the FT's coverage of Thames Water (though there seem to be more interesting questions about the financing arrangements in that case).

The second story is a GMB press release highlighting the largely foreign ownership of Anglian Water. I take my hat off to the GMB for getting some decent coverage out of something pretty straightforward - you can find the % of foreign ownership by looking on the Anglian Water website here. I think they are hitting on a vulnerable aspect of institutional investment in infrastructure in the UK - yes, there are pension funds in the mix, but they are largely overseas (thought 15% held in the UK is not insignificant).

As I've blogged before, I think this makes the politics a lot easier for advocates of public ownership of utilities. It's interesting that Anglian Water explicitly talks about who their owners are:

The point I would take from from both stories is that there is a growing argument about the nature of ownership of infrastructure. These things have always been there (well ever since the assets were sold off), they are coming to attention now because the pressure around public ownership is building.